Rising Demand for Lightweight Materials Fuels Expansion in the Aerospace Fasteners Market

Industry Overview

While the gloss of aircraft design often focuses on aerodynamics, avionics or cabin luxury, one of the unsung heroes behind every safe flight is the fastener. Aerospace-grade fasteners – from bolts and nuts to rivets and screws – make possible the assembling of fuselage panels, wings, control surfaces and interior structures. Given the demanding operational environment — extreme pressures, temperature swings, vibration, fatigue cycles and safety requirements — these components must perform flawlessly. Because of this, the aerospace fasteners market occupies a niche but vital position in the aerospace value chain.

Market Outlook

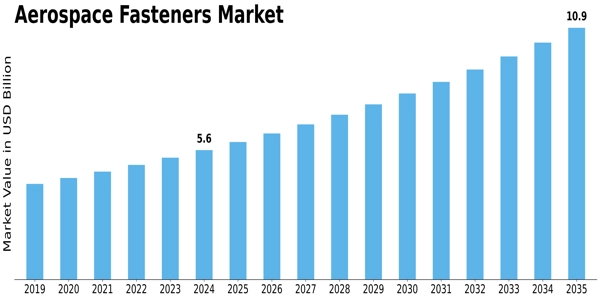

According to recent research, theaerospace fasteners market is USD 4.8 billion and is forecast to reach roughly USD 7.74 billion by the year 2030 — reflecting steady growth at a CAGR of roughly 7.0%. Growth drivers include the revival of commercial aircraft production post-pandemic, stronger defence spending in many regions, and an expanding base of regional aircraft manufacturers in emerging markets. Moreover, the push towards fuel-efficient aircraft means lighter materials and higher-performance fasteners — further elevating demand.

Key Players’ Role

Fastener manufacturers in the aerospace space are increasingly more than just commodity suppliers: they are trusted partners who must deliver certified components with traceability, consistent quality, and often custom design. Major companies — specialising in aerospace-specific fasteners and servicing Tier-1/ OEM clients — drive innovation in materials (for example titanium alloys), in production methods (such as automation and additive manufacturing) and in vertical integration. Contracting strategies often include long-term supply agreements, localisation of manufacturing to reduce lead-times, and partnerships with aircraft manufacturers to meet programme needs.

Segmentation Growth

The market segments provide insight into where growth is concentrated:

-

By product: Rivets dominate in terms of revenue – representing an estimated 65-68% share – because their reliability in aerostructure assembly remains unmatched.

-

By material: Titanium fasteners lead revenue-wise, driven by the aerospace industry's search for materials with low weight, high strength and high fatigue resistance.

-

By end-use: The fuselage category captures the largest share, reflecting the extensive fastener usage in aircraft bodies; control surfaces and interiors follow.

-

By region: North America retains dominance due to mature aerospace manufacturing and strong OEM presence. However, Asia-Pacific is the fastest-growing region, as countries such as India and China expand their manufacturing base and aviation industry footprint.

Conclusion

The importance of aerospace fasteners may not always grab headlines, but their role is critical in enabling aircraft manufacturing and performance. With rising aircraft deliveries, particularly in commercial and defence segments, and with material innovation pushing the boundaries of what fasteners must do, the market is well positioned for consistent growth. For supply chain managers, OEMs, and investors in aerospace manufacturing, the fasteners market offers both stability and a window into evolving materials and assembly technology trends.